The intention of the article is to show publicly traded companies related to sugar production and business. The article should describe each of them shortly, showing how they make money, what is the business model and what is interesting and

special in each of them. The article should be neutral, do not make any recommendations, because the goal of this analysis is to just present major sugar producers and shortly describe how companies make money on sugar productions.

The intention of the article is to show publicly traded companies related to sugar production and business. The article should describe each of them shortly, showing how they make money, what is the business model and what is interesting and

special in each of them. The article should be neutral, do not make any recommendations, because the goal of this analysis is to just present major sugar producers and shortly describe how companies make money on sugar productions.

Associated British Foods, Südzucker AG, Cosan, Adecoagro and Astarta are the sugar stocks most worth considering for international investors in 2026. Choosing between them, however, is not straightforward: each company operates a different business model, carries different currency and commodity risk, and represents a different level of pure exposure to sugar prices.

This guide breaks down the key differences using a transparent, data-driven scoring framework - so you can make an informed decision rather than guessing.

Key takeaways

- Südzucker is the largest direct sugar producer among the five stocks discussed, while Cosan’s sugar exposure comes mainly through Raízen, one of the world’s largest sugarcane processors.

- Not all sugar stocks are pure sugar plays: Astarta is highly exposed to Ukrainian sugar, Adecoagro combines sugar with ethanol and power generation, while ABF is heavily diversified through Primark, grocery and ingredients.

- Sugar stock performance depends on more than sugar prices alone, including weather, crop yields, energy prices, biofuel policy, leverage, and regional risks in markets such as Brazil, Europe and Ukraine.

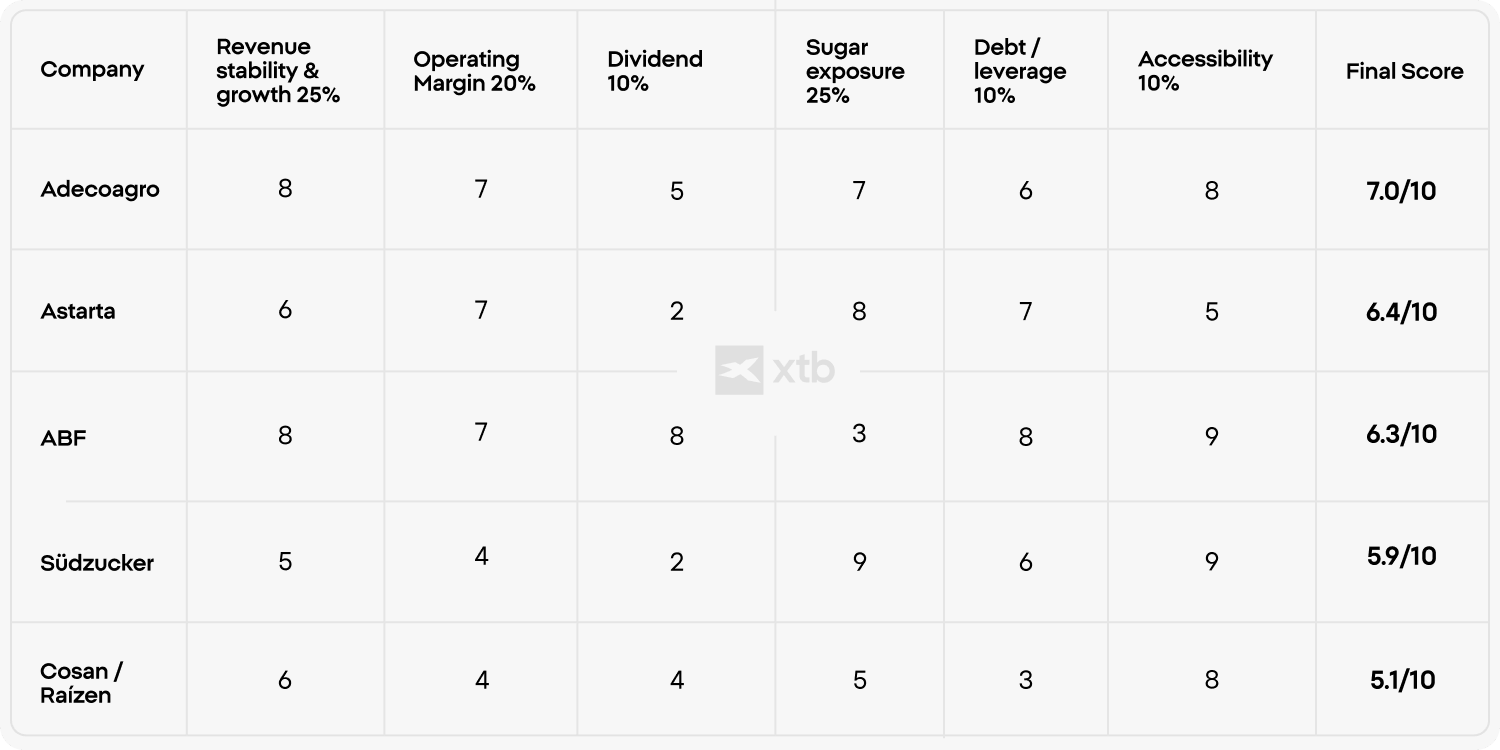

What Makes a Sugar Stock Worth Buying? Our Scoring Methodology

The sugar stocks ranking is based on a structured scoring framework designed to ensure consistency and transparency. Each company is evaluated across key financial and market

criteria, with predefined weights assigned to reflect their importance. The final ranking is driven by data, not editorial opinion, allowing for an objective comparison across the sector.

The winner in this sugar stocks ranking is clearly Adecoagro which is confirmed not only by the business quality but also by the company shares performance since the 2021 which

outperformed peers as well as major stock market indices. Remember, future outcome is uncertain, investing is risky and past performance does not guarantee future results.

Methodology Notes

- Revenue stability & growth (25%) reflects consistency and resilience over the past 2–3 years.

- Operating margin (20%) measures core profitability of the business.

- Dividend (10%) considers both yield and sustainability.

- Sugar exposure (25%) evaluates how directly a company benefits from sugar price movements.

- Debt/Equity (10%) reflects financial leverage and balance sheet risk.

- Accessibility (10%) assesses how easily international investors can access the stock (major exchanges, liquidity).

Sugar Companies: Business Models and Revenue Sources

Understanding individual sugar companies requires looking at how each of them structures its operations and where revenue actually comes from. Below is a simplified overview of how

selected companies generate revenue and what distinguishes their business models:

- Associated British Foods (ABF) – combines sugar production with large-scale food retail operations, including global brands and grocery segments, which reduces reliance on agricultural performance alone.

- Südzucker AG – focuses heavily on sugar production in Europe but complements it with bioethanol, starch, and specialty ingredients, creating a mix of industrial and food-related revenues.

- Cosan – integrates sugarcane processing with fuel distribution and logistics, linking its performance closely to both agricultural output and energy market conditions.

- Adecoagro – operates across farming, sugar, ethanol, and dairy production, with a model that depends on efficient land use and diversified agricultural output.

- Astarta – concentrates on sugar and crop production within a specific geographic region, combining farming operations with processing facilities,

Even within the same sector, companies can differ significantly in how they combine agriculture, processing, and industrial activities. This affects not only income streams but also how sensitive they are to external factors such as commodity cycles or regional conditions.

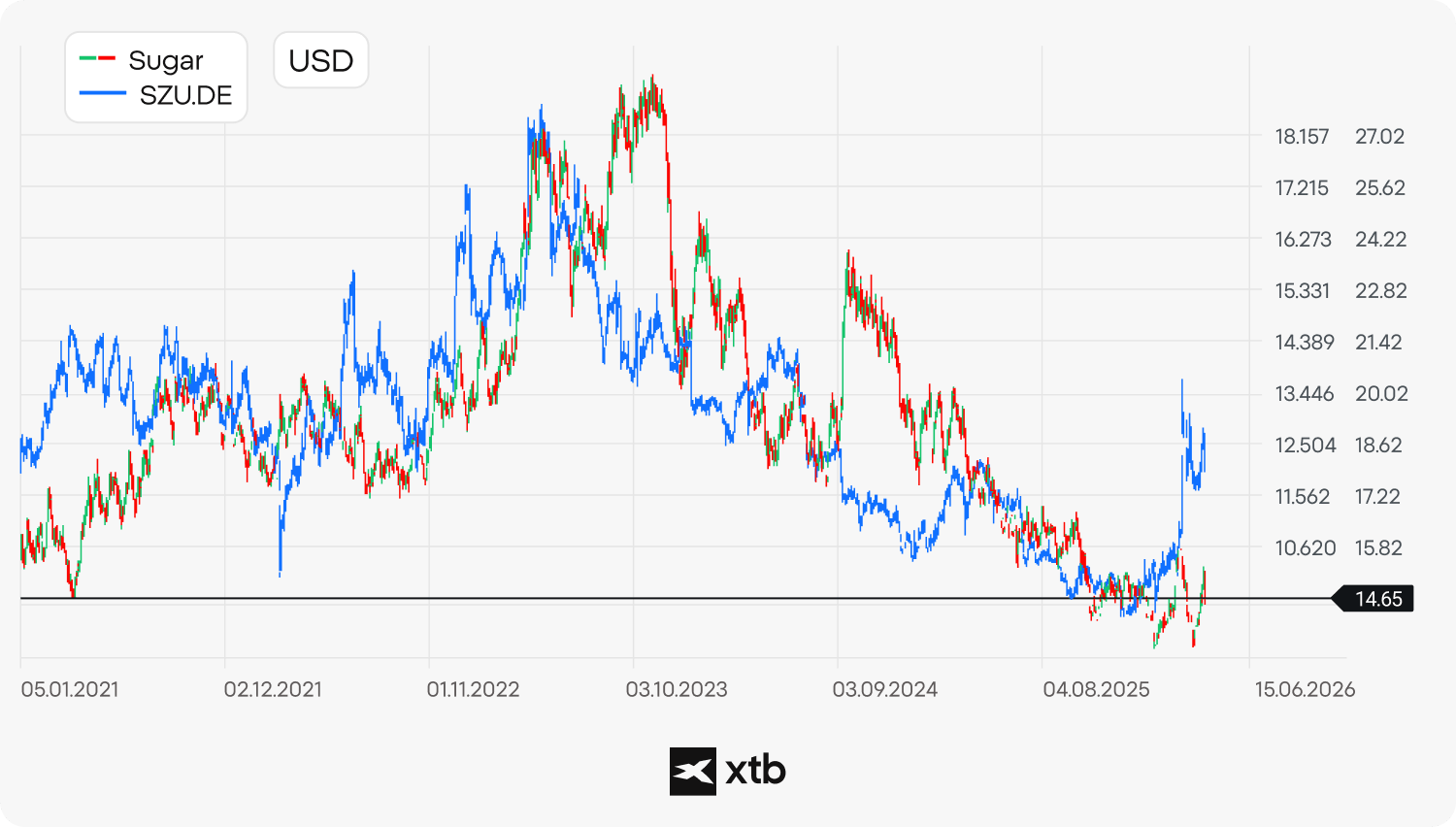

Looking at the chart we can see the stock performance of Sudzucker, Astarta Holding, Associated British Foods, Cosan SA and Adecoagro. In the given period between January 2021

- April 2026 only Adecoagro outperformed major European and American stock market indices like Euro Stoxx 50, DAX, S&P 500 or Nasdaq 100. Past performance is not reliable indicator of future results. Source: XTB Research, Bloomberg Finance L.P.

Südzucker AG - Market Position and Operational Scale

Südzucker dominates the European beet sugar market as one of the world’s largest sugar producers. The company manages a massive industrial footprint, operating over 20 sugar factories and two refineries across Europe. Annual processing capabilities reach 25–30 million tonnes of sugar beet, resulting in 3.5–4.0 million tonnes of sugar output, depending on crop yields and campaign conditions.

Key Risks:

- Cost Volatility: Fluctuations in energy and raw material costs.

- Market Pressure: Weaker European sugar prices.

- Operational Threats: Adverse weather during beet campaigns impacting yields.

- Regulatory Environment: Changes in EU agricultural policies.

Growth Catalysts:

- Pricing: Stronger European sugar prices.

- Efficiency: Improved beet yields and lower energy costs.

- Expansion: Continued growth in specialty ingredients and bio-based products, which could make group earnings less dependent on the sugar cycle over time.

Cosan - Strategic Integration and Operational Flexibility

Cosan is a Brazilian holding company with exposure to energy, logistics and agribusiness. Its sugar exposure comes mainly through Raízen, a joint venture with Shell and one of the world’s largest sugarcane processors. Raízen’s business combines sugar production, ethanol, bioenergy and fuel distribution, linking Cosan’s performance to both agricultural and energy markets. Scale is one of the key points. In the 2024/25 crop year, Raízen crushed around 77.5 million tonnes of sugarcane, although the season was affected by drought and fires in Brazil’s Center-South region.

Operational Scale and Production Outlook

Raízen operates with a significant industrial scale, though performance is subject to regional climate conditions. During the 2024/25 crop year, the company crushed approximately 77.5

million tonnes of sugarcane, a figure impacted by drought and fires in Brazil’s Center-South region. For the 2025/26 crop year, the company provides the following guidance:

- Crushing volume: 72–75 million tonnes.

- Sugar mix: 52–54% of total output.

Business Model: Commodity Flexibility.

The business model relies on operational flexibility, allowing Raízen to allocate sugarcane between sugar or ethanol production based on relative market prices. This capability serves to

optimize margins but exposes the company to specific market dependencies, including global sugar prices, ethanol demand, oil price fluctuations, and Brazilian fuel policy.

Main Risks:

- Climate volatility: Adverse weather conditions in Brazil, such as drought or fire.

- Market exposure: Fluctuations in foreign exchange (FX) rates.

- Capital structure: Corporate leverage levels.

- External environment: Regulatory changes and shifts in global energy demand.

Growth Catalysts:

- Pricing dynamics: Stronger sugar prices and higher ethanol margins.

- Regulatory support: Favorable biofuel regulations.

- Operational performance: Improved crop conditions and higher profitability across Raízen’s core segments (sugar, ethanol, and bioenergy).

Adecoagro - Integrated Agribusiness and Production Assets

Adecoagro is a South American agribusiness group with operations across sugar, ethanol, grains, rice and dairy. Its sugar and ethanol business is concentrated in Brazil, where the company operates three mills: UMA, Angelica and Ivinhema with total crushing capacity of around 14.2 million tonnes of sugarcane per year.What makes Adecoagro stand out is the flexibility of its production model. The company can adjust part of its output between sugar and ethanol depending on market conditions, usually within a 40 - 80% production range.

Production Flexibility and Performance.

The company utilizes a flexible production model, enabling management to adjust output ratios between sugar and ethanol based on market conditions, typically within a 40–80% range.

Recent production figures reflect these operational adjustments:

- 2024 Results: 12.8 million tonnes crushed; 832,389 tonnes of sugar; 532,715 cubic meters of ethanol.

- 2025 Results: 12.1 million tonnes crushed; 600,383 tonnes of sugar; 588,004 cubic meters of ethanol.

Revenue Streams and Biomass Energy.

Adecoagro integrates biomass power generation into its operational framework, creating an additional revenue stream directly linked to sugarcane processing. In 2025, the company

exported 676,389 MWh of electricity to the local grid, enhancing its income diversification beyond raw commodity sales.

Main Risks:

- Environmental: Adverse weather conditions in Brazil affecting crop yields.

- Market: Price spread volatility between sugar and ethanol.

- Economic: Currency volatility and broader macroeconomic exposure in South America.

Growth Catalysts:

-

Pricing: Potential for stronger sugar prices.

- Demand: Rising ethanol demand.

- Regulatory: Supportive biofuel policies.

- Efficiency: Higher crop yields and improved industrial capacity utilization.

Associated British Foods (ABF) - Group Structure and Diversification

Associated British Foods is a diversified conglomerate spanning five segments: sugar, grocery, ingredients, agriculture and retail. Sugar accounts for only one part of the group's revenue base, with Primark — the value fashion retailer — acting as the primary earnings driver. This multi-segment structure means weakness in one division is partially offset by performance elsewhere, reducing ABF's sensitivity to agricultural cycles.

The group's sugar operations are conducted through AB Sugar — ABF's dedicated sugar division — which runs 29 processing plants across 10 countries and employs approximately

40,000 people. Its footprint includes the UK, Spain, southern Africa and China, giving thecompany exposure to different crop cycles, sugar markets and regulatory regimes. In the UK,

British Sugar remains a key producer, although output can vary sharply with weather conditions; in FY2023, UK sugar production fell to around 0.74 million tonnes after a difficult beet harvest.

Main Risks

- Weather: beet harvest volatility directly impacts UK sugar output (FY2023: 0.74mt vs.normalised ~1mt+)

- Market: lower European sugar benchmark prices compressing AB Sugar margins

- Macro: FX exposure across multiple operating currencies

- Retail: margin compression in Primark from input cost inflation and consumer spending shifts

- Regulatory: evolving agricultural policy across ABF's 10 sugar-producing markets

Growth Catalysts:

- Primark international expansion reducing UK revenue concentration

- Sugar price recovery in European and global markets

- Efficiency gains across AB Sugar's multi-country plant network

- Improved UK beet yields following adverse 2023 harvest season

Astarta

Astarta is a Ukrainian agribusiness company focused on crop production and sugar processing. Its integrated model combines farming, logistics and industrial refining, giving the company exposure to sugar prices, beet yields, input costs and local infrastructure conditions. Annual sugar output has generally ranged between 220,000 and 300,000 tonnes since 2020, with a dip in 2022 following Russia's full-scale invasion of Ukraine. Production later recovered as export routes and operating processes adjusted.

Main Risks

- Geopolitical: active war affecting transport routes, energy costs, labor availability and financing conditions

- Logistics: Black Sea route disruptions forcing reliance on costlier overland EU transit

- Market: sugar price volatility and beet yield sensitivity

- Macro: restricted access to export markets and elevated operating costs across the supply chain

Growth Catalysts:

- Ceasefire or peace agreement reducing operational disruption and financing costs

- Lower logistics costs as export route conditions normalise

- EU accession progress expanding Astarta's addressable market for Ukrainian sugar

- Improved trade stability through deeper Ukraine–EU agricultural integration

Who Actually Produces the Most Sugar? The Biggest Companies by Volume

The largest listed sugar stocks are not always the largest sugar producers. Many of the biggest players are private, cooperative-owned, or listed on less accessible exchanges, while others

such as ABF or Wilmar are diversified groups where sugar is only one part of the business. By volume, Südzucker is one of the largest listed beet sugar producers globally, with annual

output of around 3.5 to 4 million tonnes. AB Sugar, part of Associated British Foods, operates across Europe, Africa and the Americas, making it one of the most geographically

diversified sugar businesses.

Raízen, backed by Cosan and Shell, is one of the world’s largest sugarcane processors and

exporters, although its production is split between sugar and ethanol depending on market conditions. Other key players include Tereos, a major French cooperative active in Europe and

Brazil, and Mitr Phol, the largest sugar and bioenergy producer in Asia, which remains privately owned.

The U.S. sugar market is dominated by private companies and farmer cooperatives, which limits direct exposure for public equity investors. Key producers include U.S. Sugar

Corporation (700 tonnes annually), American Crystal Sugar Company (appx. 15% of national sugar supply) and Imperial Sugar. Public companies such as Bunge and Archer Daniels

Midland (ADM) are often mentioned in agricultural markets, but they are not major world-class sugar producers.

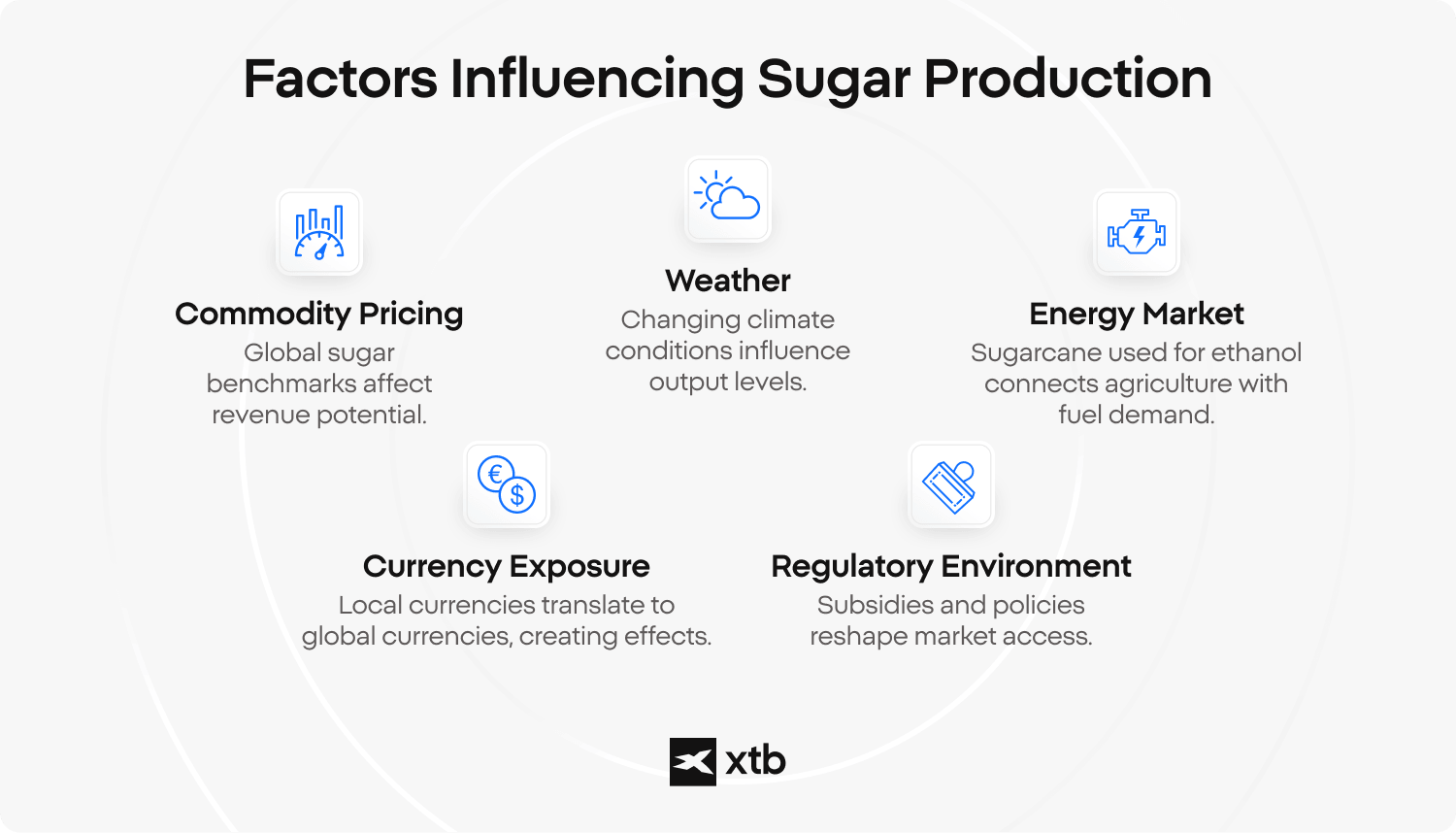

What Factors Drive Sugar Stock Performance?

Sugar stocks are influenced by far more than the headline sugar price. Margins, crop yields, energy markets, currencies and trade policy can all change the outlook for producers quickly,

making the sector highly cyclical and sensitive to global supply conditions.

- Global sugar prices (ICE futures): Benchmark prices directly impact producer margins. When sugar prices fall, revenues and profitability typically come under pressure across the sector.

- Weather and crop conditions: Sugar supply is highly sensitive to climate. Droughts in Brazil or floods in India can quickly tighten global supply and trigger sharp moves in both sugar prices and related equities.

- Sugar vs. ethanol allocation (Brazil): In Brazil, mills can shift sugarcane between sugar and ethanol production. Higher oil prices often increase ethanol demand, reducing sugar supply and supporting sugar prices.

- Currency movements: Many producers operate in currencies such as BRL, THB or INR, while sugar is priced globally in USD. Exchange rate fluctuations can significantly impact reported earnings and cost competitiveness.

- Government policy and trade regulation: Subsidies, export controls and import tariffs (notably in the EU, India and the US) can distort supply-demand dynamics and influence both pricing and company valuations.

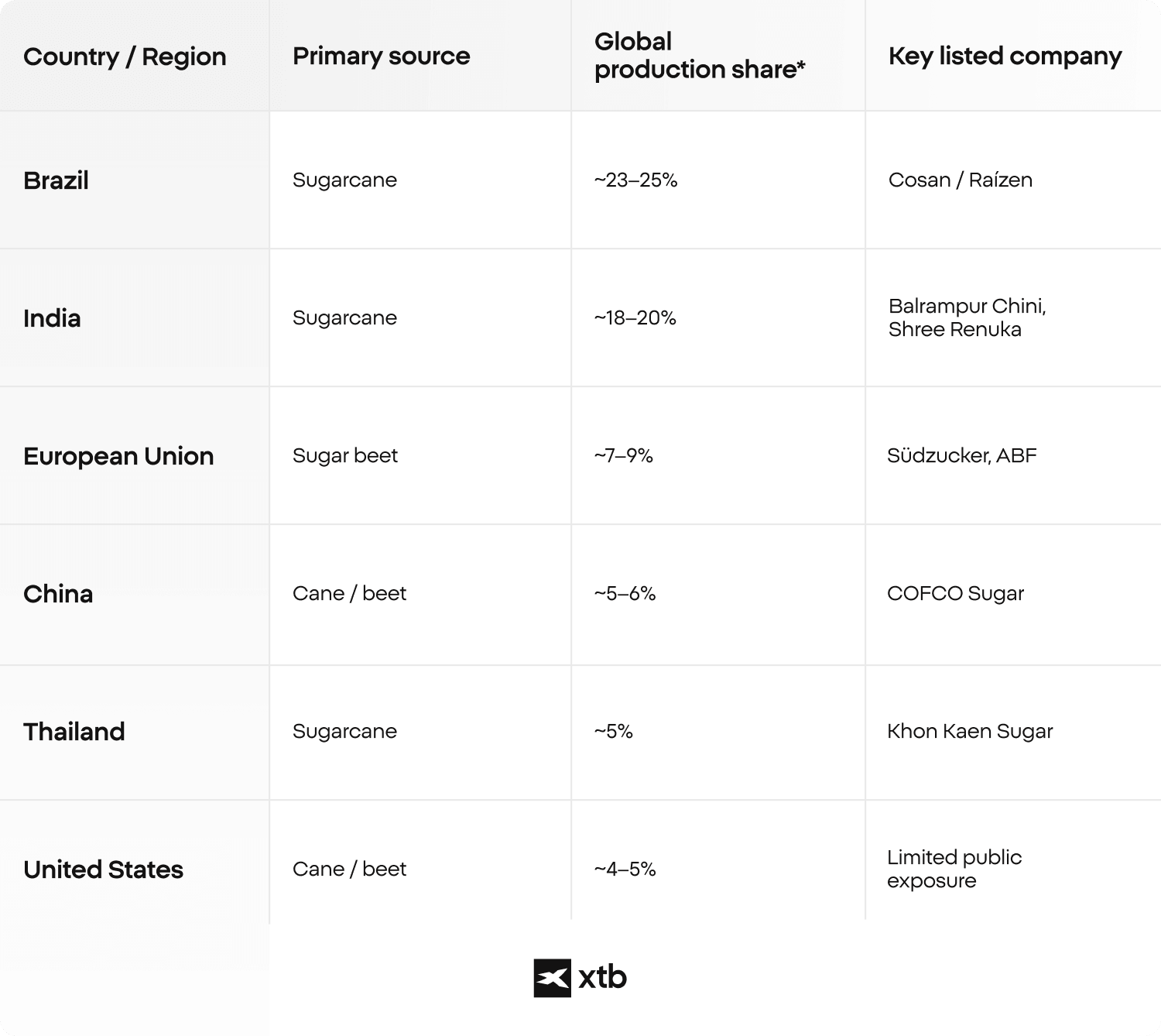

Which Countries Dominate Global Sugar Production?

Global sugar supply is concentrated in a handful of regions, but the largest producers are not always the most accessible for investors. Here is the breakdown of countries dominating global sugar production at scale with Brazil, India and EU leading the market.

Approximate shares based on recent USDA global production estimates (189.3 million tonnes annually in 2025/26 season). Brazil is forecast at 44.7 million tonnes, India at 35.25 million

tonnes, the EU at around 15 million tonnes, China at 11.5 million tonnes, Thailand at 10.25 million tonnes, and the U.S. at 8.42 million tonnes. Values vary by season depending on weather and policy.

FAQ

Sugar stocks are shares of companies involved in producing, processing, or distributing sugar and related products. They represent businesses rather than the raw commodity itself, which means their performance depends on operational factors, costs, and strategic decisions, not just sugar prices. In practice, this often includes companies that also produce ethanol, food ingredients, or energy.

No, sugar stocks do not move in perfect alignment with sugar prices. Company performance can diverge due to costs, currency effects, or diversification into other business areas.

For example, a company may face higher production expenses even when sugar prices are rising, which can limit the impact on its financial results.

A large portion of global sugar production is controlled by private companies or cooperatives.This means that the biggest producers are not always accessible through stock exchanges, which can create a gap between global supply leaders and investable companies. As a result, publicly traded sugar stocks represent only part of the overall industry.

In some regions, especially Brazil, sugarcane can be used to produce either sugar or ethanol. This flexibility allows companies to adjust production based on market conditions, linkingtheir performance to both agricultural and energy markets. When fuel demand rises, moreoutput may be directed toward ethanol instead of sugar.

Sugar stocks are often grouped within commodity-related equities, but they are not pure commodity instruments. They combine exposure to raw materials with business operations, meaning their behavior reflects both market prices and company-specific factors such as efficiency and diversification.